SBA and Conventional Interest Rates: Current, Past And Future

Fixed Rates

Standard conventional fixed rate loans from the lenders we work with are set at a spread between 300 and 350 basis points over the 10 year treasury rate (currently 3%). The size of the loan amount does not automatically place a borrower in a particular rate, the quality of the loan and strength of the borrower (or lack thereof) are larger factors influencing the rate provided.

Most SBA lenders don’t offer fixed rates but when they are available the range must still comply with the SBA maximum rate guidelines. SBA 7(a) standard loans fixed rates cannot be higher than 2.75% over the Wall Street Prime Rate which is currently at 4%.

Variable Rates

Most SBA 7(a) loans are structured as a variable rate loan. Most all SBA lenders will charge a variable rate from 2% to 2.75% above the Wall Street Prime Rate.

Wall Street Prime Rate

The Wall Street Prime rate is the base rate typically used by SBA lenders. The WSP rate goes up or down based on the Federal Reserve’s prime rate. The rule of thumb is the WSP rate will be 3% higher than the Fed rate. Currently the WSP rate is 4%.

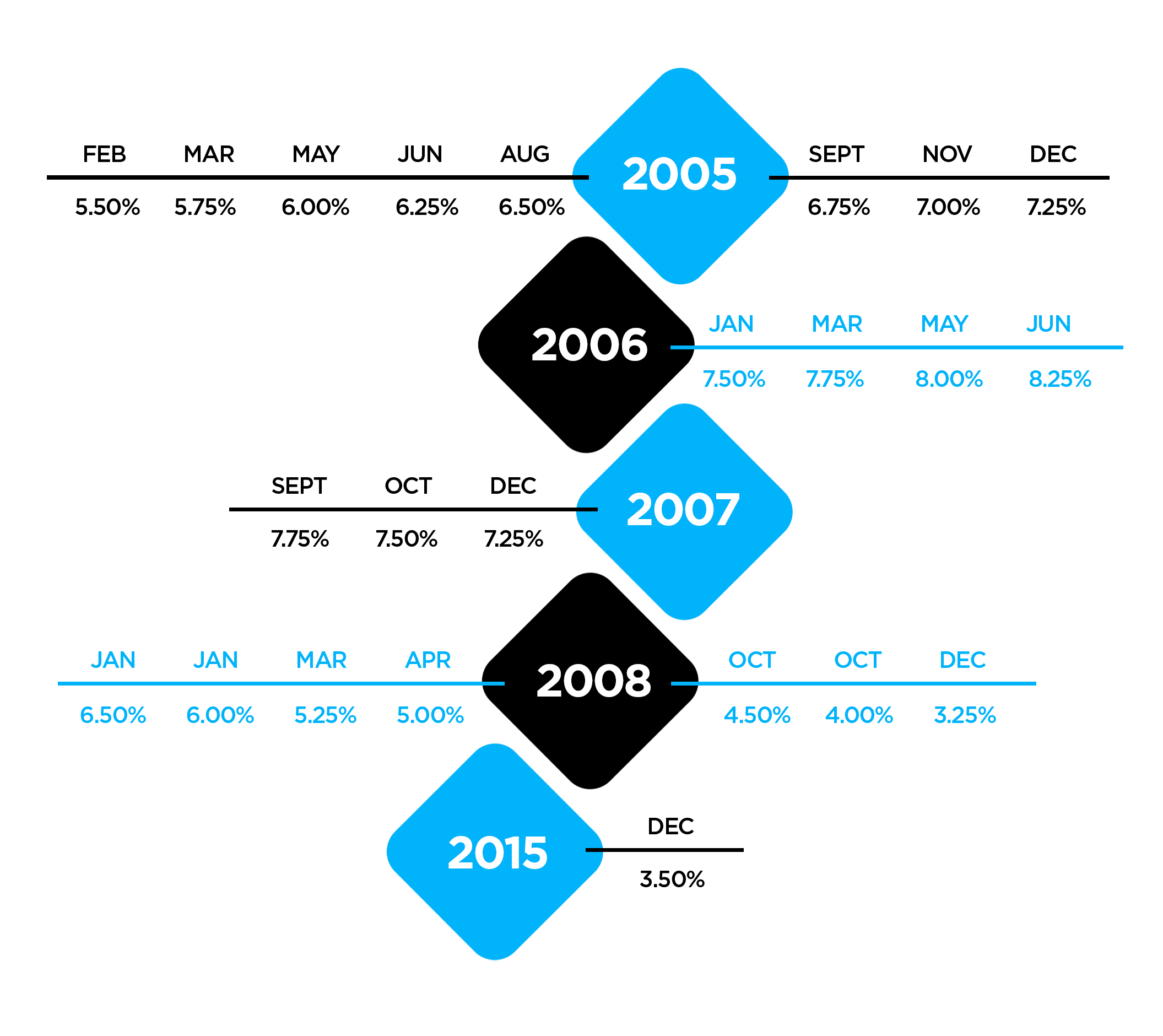

Comparing the Current WSJ Prime Rate to Years Past

The current (May 2022) WSJ Prime Rate is 4% which is higher than the 3.25% that was in place late March 2020 to March of 2022. However, this is still a historically competitive rate, even in recent years. The WSP rate was 5.5% in December 2018, 4.75% in December 2019, and 4.25% in early March 2020.

Factors Impacting Rate

Lenders will adjust their preferred rate up or down primarily based on strong cash flow, net worth, loan size, and any prior loans or experience with the borrower. Usually, we see the lenders with the widest qualifying criteria aren’t the lowest rate lenders and the lenders with narrower criteria standards offer slightly lower rates.

How important is rate compared to other factors?

Considering that both conventional and SBA lenders are generally going to be within 25 to 75 basis points of each other for the same loan and program being equal, there isn’t a “drastic” difference in rate between lenders that are focusing on the wealth management industry. Of course, the lower the rate the better but the cost of the loan isn’t usually a nigh and day difference between most of the lenders focused in the wealth management industry niche.

For example, this is the difference a 25 basis point increase makes to the monthly payment for a $1 million loan on a 10 year term:

6.00% = $11,102 mth payment

6.25% = $11,228 mth payment

6.50% = $11,354 mth payment

6.75% = $11,482 mth payment

7.00% = $11,610 mth payment

The more important factors than rate for most borrowers will be the lender’s qualifying criteria, their expertise and experience in wealth management M&A, how dialed in the lender is with process and support, if there will be collateral requirements, what the lender’s long term commitment is to the advisor lending space, the willingness to approve and fund multiple acquisitions, the cash down payment and seller financing requirements and flexibility, and the lender’s ongoing required covenants imposed on the borrower.